Can Apollo Fight Online Education Any Longer?

Confira nosso artigo (27/3/2015) no Seeking Alpha: Can Apollo Fight Online Education Any Longer?

Clique aqui para ler, comentar, e opinar diretamente no Seeking Alpha.

Summary

- Online courses are rapidly growing; this is good news for many educational bodies, but not Apollo.

- Revenues and profits are dwindling; prices have plummeted below all analysts’ expectations.

- At current prices, our algorithmic analysis is bullish on Apollo, in contrary to most investors and analysts.

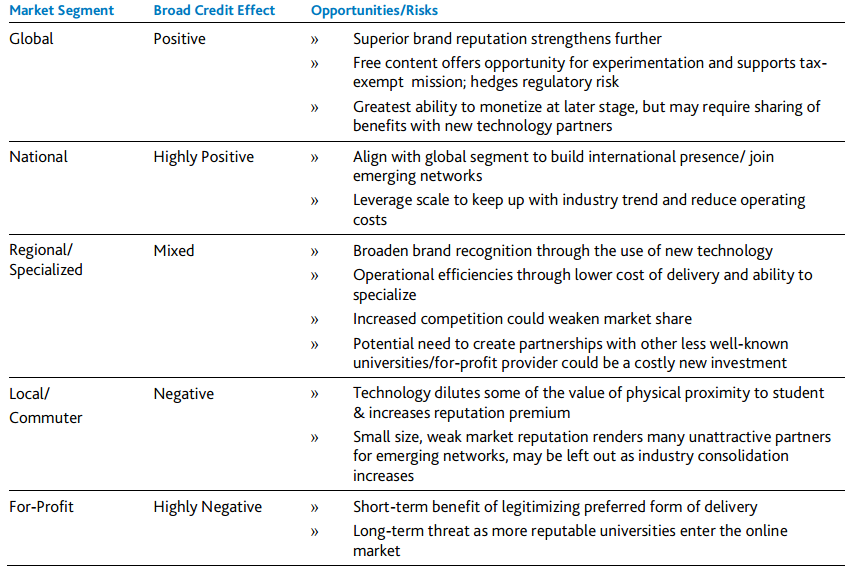

Online Courses are Likely to Shape the Future of Education

While most elite non-profit universities such as Harvard and Duke might benefit from the emergence of online courses, private for profits could very well find themselves squeezed out. Most importantly, the acceptance of online education by these elite bodies, such as in the example of Coursera and edX, will legitimize this form of education very quickly. However, smaller colleges that are not a part of these high-reputation online networks are about to face a serious challenge in coming years. In the online report “Shifting Ground: Technology Begins to Alter Centuries-Old Business Model for Universities,” Moody’s outlines who will benefit and who will lose from this transition to online courses.

(click to enlarge)

Apollo Education Group

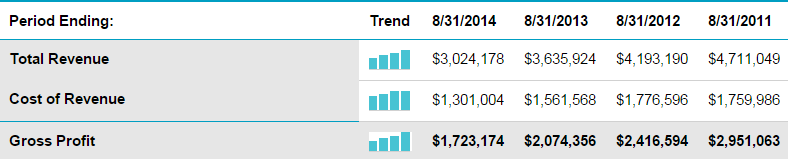

One of the largest for-profit institution that has begun to feel this demand crunch is the Apollo Education Group (NASDAQ:APOL), which owns and operates four higher education institutions: the University of Phoenix, Western International University, Axia College, and the College for Financial Planning. It also owns various colleges internationally as a part of the Apollo Global group. To say that the education group is doing badly would be a serious understatement. Net revenue in fiscal year 2011 was $4.7 billion. Just one year later, revenue dropped to $4.2 billion. In 2013, net revenue was $3.6 billion, and in 2014, just $3 billion.

(click to enlarge)

The latest statement regarding the group came from Bank of America. After setting a price target of $24, the bank added, “While the trajectory of starts remains uncertain, we do expect improvements with the lap of the LMS rollout (mid 4Q15) and continued progress at Apollo Global (11% of FY14 revenue).” The ApolloLMS system is an online management system designed to take care of course management, online testing and results, generating certificates and management of events and users. While this sounds promising as a way out of the slump, it is hardly revolutionary. Moodle is a free open source code integrated in most European universities – which does just that. What perhaps is the truly attractive sector is Apollo Global.

The target countries are generally ones transitioning into a larger middle class, and are thus beginning to offer government aid to attend for-profit colleges, similar to the U.S. system. These countries are rapidly growing and their education needs are as well. Brazil, South Africa, and India are major targets for such growth in the coming years. The relatively low regulations will also allow Apollo to have much freedom in their planning, hiring, and educational programs, a significant advantage over the strongly regulated U.S. market.

Why Apollo is Still Attractive… Maybe

Apollo is an old group. Founded in 1973, the company has amassed a massive 40 years of experience in the for-profit education market; moreover, education demand is growing globally, not declining. From a fundamental perspective, in an industry like this, experience means a lot. After viewing the numbers at the top, one might conclude that the company is going bankrupt; however, quite the contrary is true. Although the 1st quarter of 2015 was less than impressive, the previous three were profitable.

(click to enlarge)

Secondly, the company has a stable balance sheet. Total assets as of Feb 28, 2015 are valued at 2.4B, of which 1.4B are current assets. Total liabilities are 1.2B with 900M being current. This makes for an enterprise value of 1.37B (according to Yahoo Finance) with a current market cap of 2.08B. Thus investors are looking at $710m of equity which is truly at risk. If we divide that $710m by the 95m Apollo earned in the last 4 quarters we get 7.4 years’ worth of earnings at the current rate. This seems very cheap, and it is. Assuming ApolloLMS creates any sort of growth and profits, and that Apollo Global expands as expected, the stock will likely appreciate back to the $32 level it had prior to the last financial report.

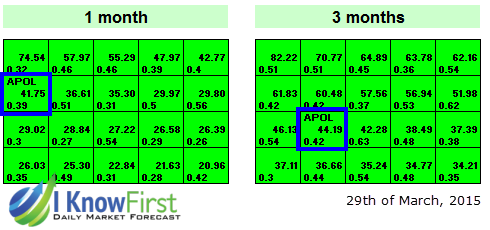

The market forecast self-learning algorithm at I Know First affirms the bullish outlook for Apollo. I Know First says Apollo has one of the strongest Buy signals for the 1-month and 3-months horizons. The positive +41.72 and +44.19 algorithmic signal say Apollo is currently undervalued, and bottom numbers 0.39 and 0.42 indicate it has a very high probability of going up in price over these periods.

Conclusion

It is tough to write a definite opinion here. Apollo is an experienced, well established, for-profit educational body. The company recognized that its U.S. operations, its bread and butter for many years, is now slowly dwindling down. With increased efforts into its online integration and expansion into global markets, the company might be able to offset these losses, which will likely cause the stock’s price to soar. This new model could have so much success that the company’s growth might exceed its previous operation size – which was largely depended on the University of Phoenix as the stone pillar holding it together. So, will Apollo succumb to the power of the Internet as so many brick and mortar businesses did before, or will it adapt and come out stronger than it originally was? That is indeed the question on which this investment hangs. One thing is certain, current price levels reflect investors do not believe Apollo will make this recovery, which is what sets it up as an attractive opportunity for growth.