Citigroup: Cheap For A Reason?

Confira nosso último artigo (03/08/2014 )no Seeking Alpha: Citigroup: Cheap For A Reason?

Clique aqui para ler, comentar, e opinar diretamente no Seeking Alpha.

Summary

- Strong second quarter earnings and low P/B and P/E ratios make Citigroup an attractive stock.

- Citi is expanding its business in Asia-Pacific region, while its branches in Russia are contracting due to conflict with Ukraine.

- In order for Citigroup to return more capital back to its shareholders, the bank must pass the next annual stress test.

- C shares are forecasted to fall in the 1-month, 3-month, and 1-year time horizons according to the I Know First Algorithmic Forecast.

Introduction

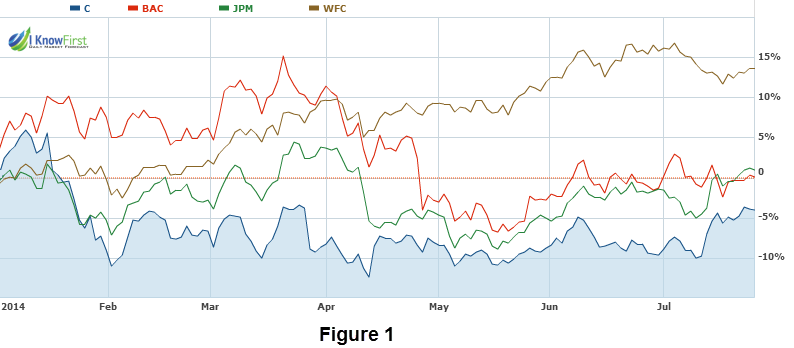

Citigroup (NYSE:C), the American multinational banking and financial services giant, recently reported solid second quarter results on July 14th. Over the past few weeks, the company’s stock price has gained 5.97% (July 10th – July 28th). However, this recent surge is far from the norm. Citigroup has struggled to keep up with its competition since the start of the year, as seen in the figure 1.

(click to enlarge) Below, I have conducted a SWOT analysis, noting the strengths and weaknesses of Citigroup, as well as the opportunities and challenges that lie ahead. In addition to this analysis of Citigroup, recent articles on JP Morgan(NYSE:JPM) and Bank of America (NYSE:BAC) can also be found on ourauthor page.

Below, I have conducted a SWOT analysis, noting the strengths and weaknesses of Citigroup, as well as the opportunities and challenges that lie ahead. In addition to this analysis of Citigroup, recent articles on JP Morgan(NYSE:JPM) and Bank of America (NYSE:BAC) can also be found on ourauthor page.

Strengths

One of Citigroup’s greatest strengths is its low Price/Book ratio of 0.74, meaning that the bank’s stock is currently valued at 73% of the total value of the company’s assets. Citigroup is the only big bank to trade below its tangible book value. This demonstrates that the market is bearish on Citigroup, which could lead to some massive growth with the right catalyst.

The bank’s low P/E ratio of 11.06 further supports this conclusion. This figure is significantly lower than Citigroup’s competitors, with Bank of America and JP Morgan posting 19.45 and 13.99, respectively. While Citigroup no doubt has its issues, the current stock prices make the bank an attractive buy.

The bank’s second quarter earnings were a step in the right direction, with adjusted earnings up 1% to 3.93 billion, or $1.24 per share. Analysts had expected adjusted earnings of $1.05 per share, making it a big beat for the bank on that metric.

Weaknesses

As the U.S. housing market recovers, the demand for mortgage refinancing weakens. Additionally, the banking sector still remains sluggish, with global consumer banking revenues down 3% to 9.4 billion for Citi. Despite the U.S. economy’s recovery from the financial crisis, the company is still suffering from the stock dilution experienced in 2009. Few companies had been as badly damaged by the financial crisis as Citigroup, and the company is still feeling the effects of the $58 billion stock exchange.

Despite Citigroup’s strong earnings of $4.35 per share, the company’s revenues have continued to lag behind. The bank’s quarterly revenue growth (yoy) has been on the decline, down 5% for the past 12 months, compared to Bank of America’s 1% drop in revenue growth.

According to our algorithmic forecast, Citigroup is a strong sell in the 1-month, 3-month, and 1-year timeframes. Since the forecast, Citigroup has already fallen nearly 4%.

At I Know First, we utilize an advanced self-learning algorithm based on Artificial Intelligence [AI] and Machine Learning [ML] that also incorporates elements of Artificial Neural Networks as well as genetic algorithms in order to model and predict the flow of money in almost 2,000 markets from 3 days to a year. As such, we promote algorithmic trading coupled with a vigilant risk management strategy and fundamental analysis for avant-garde investment strategies designed to mitigate maximum amount of risk as well as to optimize potential returns. Just to be clear, this is not high frequency trading, and the differences are explained here.

The market prediction system is entirely empirical and not based on human-derived assumptions. This system can also be referred to as a “Big Data” solution for Wall Street by incorporating popular types of convergence averages and moving averages that have been traditionally used to forecast assets with complex and intelligent algorithms that can make these predictions more accurate and efficient.

The human factor is limited to building the mathematical framework and initially presenting the system with the “starting set” of inputs and outputs, which is also utilized for recognizing every other market opportunity. The algorithm then repetitively proposes “theories” and recurrently tests them automatically on years of daily market data. It then validates them on the most recent data, which prevents over-fitting. By separating the predictable part from stochastic (random) noise, the algorithm is able to create a model that projects the future trajectory of the given market in the multi-dimensional space of other markets. The output of the predicted trend is a number, known as the signal, which is used by traders to identify entry and exit points in the market. While the algorithm can be used for intra-day trading, the predictability tends to become stronger over longer time horizons, such as the 1-month, 3-month and 1-year forecast, making this market prediction system ideal for longer-term trading.

The color-coded forecast (figure 2) above is very easy to read. Deeper greens signify that the algorithm is very bullish, and vice-versa for deeper reds. The signal is the number flush right in the middle of the box and is predicted direction (not a specific number or target price) for that asset, while the predictability is the historical correlation between the prediction and the actual market movements. In other words, the signal represents the forecasted strength of the prediction, while the predictability represents the level of confidence. These are two independent indicators, but consider both as you make your own analysis. In this instance, Citigroup has a strong negative signal of -65.22 and predictability of 0.21 for the 1-month forecast, meaning that the algorithm is extremely bearish on the bank. Further explanations are available here.

Daily forecasts are intended to be utilized as a tool to enhance portfolio performance, verify their own analysis and act on market opportunities faster. We never recommend blindly purchasing assets that are endorsed by the algorithm without your own additional analysis.

Opportunities

With Citigroup trading at such a discount, there is the potential for a huge return. The stock price can go up 50% just by realizing the company’s book value. Citi is forecasted to increase EPS by 50% next year, which would give free up more capital to distribute to shareholders through dividends and buybacks, as well as help the bank realize its book value. However, this is all dependent on Citigroup passing the fed’s stress test.

Looking into the future, the U.S. economy and banking sector looks like it’s on the right track. As the housing market and economy continue to improve, there is a good chance that Citigroup will have excess reserves. This may help bring back the investor confidence that the company has been struggling to find as of late. The mortgage-backed security market is also beginning to heat up again, and Citigroup will no doubt have a hand in that.

On the international front, Citigroup is expanding its commercial banking operations in the Asia-Pacific region, as the bank intends to hire 100 new bankers in Asia, representing a 10% increase in the region’s employee base. The company aims to provide an array of products to corporate clients with annual sales ranging $10-$500 million. Citigroup is not alone in its venture further into Asia-Pacific, as HSBC Holdings plc has already implemented a similar strategy. Both of these companies have traditionally thrived on multi-billion IPO deals from Chinese-state owned companies. However, these value deals are becoming less common, and the future seems to lie in capturing small to medium sized enterprises.

Threats

After failing the Federal Reserve’s annual “stress test,” Citigroup is now forbidden from raising its dividend or increasing its stock buybacks. The bank fell short in its assessment of the risks it faced during a scenario of sustained economic stress. If the restrictions on the bank’s dividends and buybacks were not enough to deter investors, it certainly is not comforting to know that Citigroup’s business model would not be able to sustain another financial crisis.

The international landscape is not all sunshine and rainbows for Citi, as instability in Russia and unrest in Ukraine continues to escalate. As a result, more and more U.S. banks are reducing exposure to the nation. Citigroup’s total exposure fell 5.3 percent to 8.9 billion in the 3 months ended June 30th. Citigroup currently has more than 50 branches in Russia, and the continued conflict will no doubt negatively affect the New York-based bank’s profitability.

Conclusion

At first glance, Citigroup may appear to be an undervalued gem. With nice second quarter earnings report and stellar recent gains, many may see the company as having a bright future. However, there is a reason the stock remains a bargain. The Federal Reserve has its thumb on the bank’s future, restricting any further increases in dividends or stock buybacks. With no major catalysts on the bank’s horizon, I see no reason to take the risk of holding this underperforming bank. In this instance, I would agree with the algorithmic forecast and stay clear of Citi for the time being.

Business disclosure: I Know First Research is the analytic branch of I Know First, a financial startup company that specializes in quantitatively predicting the stock market. Joe Stempel, an I Know First intern wrote this article. We did not receive compensation for this article (other than from Seeking Alpha), and we have no business relationship with any company whose stock is mentioned in this article.