Tesla Stock Forecast For 2015 Based On A Predictive Algorithm

Confira nosso artigo (31/12/2014) no Seeking Alpha: Tesla Stock Forecast For 2015 Based On A Predictive Algorithm

Clique aqui para ler, comentar, e opinar diretamente no Seeking Alpha.

Acompanhe a performance de nossos artigos.

Summary

- Tesla Motors, Inc. is an American company internationally renowned for its electric vehicles and electric powertrain components.

- Recently, while the company has experienced consistent growth for the last two years, share prices temporarily dipped in response to problematic business for Tesla China, alongside lowered analyst estimates.

- Despite this, Tesla Motors is a stock worth considering: while it may fluctuate in the short term, it restores itself via its business developments, unique organizational structure, and innovative leadership.

- The I Know First algorithm predicts a bullish forecast for Tesla in the three-month time frame.

Company Profile: Tesla Motors, Inc.

“As in nature, all is ebb and tide, all is wave motion, so it seems that in all branches of industry, alternating currents – electric wave motion – will have the sway.” – Nikola Tesla, physicist, electrical engineer, and inventor of alternating current machinery

Tesla Motors, Inc. (NASDAQ: TSLA) is an American company that – like the Serbian-American inventor after whom it is named, and from whom it gets its AC motor – needs nearly no introduction: taking Nikola Tesla’s above-quoted claim that electricity trumps everything (gasoline included) to heart, Tesla Motors has, in its own words, “set out to prove that electric vehicles [can] be awesome.” Headquartered in the technologically industrious city of Palo Alto, California, the company serves Canada, Western Europe, the Middle East, China, Japan, Australia, and New Zealand. In particular, Tesla Motors managed to gain widespread recognition in 2008, when the Tesla Roadster – the world’s first entirely electric sports car – initially entered production; since then, Tesla Motors has been consistently hailed by those interested in luxury automobiles as a conceptually innovative, technologically cutting-edge, and operationally unique creator of electric cars and electric vehicle components. More specifically, in recent years, with its share prices increasing dramatically in 2013, its CEO’s being recognized as a man about whom history books will be written, and its newer Model S routinely bringing home sizable distinctions, including Motor Trend’s prestigious 2013 Car of the Year award, Tesla – while it remains only approximately forty percent the size of Ford (NYSE:F) – has tended to receive considerably positive attention from investors: so much so, in fact, that it has been colloquially termed “the darling of Wall Street”.

Recent & Current Events: The 2013 Boom, Continuing 2014 Success, and the December Drop

As our introduction suggests, then, the recent past has been relatively kind to Tesla Motors: share prices have been increasing consistently for over five years (Figure 1), and they have jumped most significantly over the course of the last two years. Despite a short-term tumble caused by comparatively disappointing third-quarter results, 2013 – now referred to by many investors as Tesla’s “best year yet” – saw TSLA stock surge more than fivefold (Figure 1), culminating in a 350 percent increase (an increase, it should be noted, about ten times that of both General Motors Co. (NYSE:GM) and Ford Motor Co., each of which went up by only 30 percent or so in 2013).

(click to enlarge)

Figure 1 (above). A Yahoo! Finance five-year historical chart tracking Tesla Motors’ prices: since approximately 2010, the company has, holistically speaking, seen an upward trend. Note, too, that share prices experienced particularly prominent increases in 2013.

This year, share prices continued to increase, though considerably less spectacularly than they did in 2013: while 2013 prices shot all the way from $32.91 in January to $190.90 in September, this year has had a comparatively modest 52-week range ($139.34 to $286.04, once again in January and September respectively), and a couple of noticeable drops (Figure 2).

(click to enlarge)

Figure 2. Tesla Motors’ share price fluctuations across 2014: prices consistently remained in the $130.00 to $290.00 range.

One such drop, as the above diagram indicates, occurred relatively recently: shares of Tesla fell more than 15% in the two weeks preceding December 12th, closed below $200 for the first time since May on December 16th, and slid to a seven-month low of $192.65 on December 17th; this presumably occurred in response to, among other things, a Tesla China chief’s resignation, and Morgan Stanley analyst Adam Jonas’s lowered Model 3 volume and price target estimates. This dip, however, didn’t taint Tesla’s shares for very long: by December 18th, share prices had been restored to – and had managed to exceed – pre-drop levels; since, they’ve again climbed, peaking at $227.82 on Boxing Day.

Why did Tesla so rapidly achieve renewed support, however? Most of us believe the company to be a worthy long-term investment, to be sure, but why did the market jump to restore Tesla share prices within, essentially, two days? Among other reasons, it seems that CEO Elon Musk’s Christmas Day Twitter activity (detailing a plan to upgrade the battery on the Tesla Roadster – the company’s first production vehicle – and thus upgrade its travel range) and Stifel Nicolaus analyst James Albertine’s revised Boxing Day price target (upgrading Tesla shares to the highest target on Wall Street) may be responsible.

With both negative and positive events to its name as of late, Tesla Motors, Inc. is currently trading at a value that, in the context of the stock’s yearly performance, could be seen as a decent intermediate: $225.71.

The Positive Attributes

As could be anticipated in light of recent events, Tesla – though it remains highly regarded for the most part – has been the subject of some criticism this month. While it is important to confirm that a company is sufficiently realistic in its self-evaluation, and that public perception hasn’t “jumped the gun”, it seems that, at present, there exist significantly more positive than negative facets to Tesla. Namely, Tesla’s revenue and profit growth, elevated production goals, lack of competition, recent business developments, unique organizational structure and leadership, and ability to problem-solve are all key to the supposition that Tesla has a decently bright future.

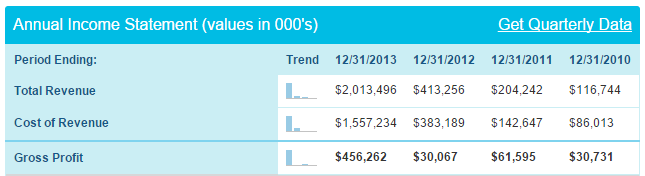

To begin, Tesla’s revenue and gross profit have increased every year since 2010 (Figure 3), with the most recent years yielding the best results. 2013, for example, was particularly eventful. As can be seen on the NASDAQ graphic below, both annual revenue and annual gross profit increased dramatically in that year – total revenue was $2013.496 million (up from $413.256 million in 2012), and gross profit was $456.262 million (up from $30.067 million in 2012). 2014 has continued to see Tesla grow where these numbers are concerned: while annual revenues and gross profits have not as yet been computed for 2014, given that we’ve Q4 to finish, it appears that they will exceed last year’s. According to Tesla filings, all of the first three quarters of 2014 saw year-over-year growth in both revenues (Q1: 10%, Q2: 89%, Q3: 97%) and gross profits (Q1: 61%, Q2: 111%, Q3: 144%), with each new quarter seeing larger year-over-year gains than the preceding one (Figure 4), and Q3 dramatically exceeding analysts’ estimates (while Bloomberg consensus-predicted zero cents, earnings ended up being two); assuming that this trend continues, this year’s cumulative outcomes are likely to top 2013’s. In fact, simple addition suggests that they already do: Tesla’s summed Q1, Q2, and Q3 2014 revenues ($2241.605 million, approximately) already exceed the company’s total 2013 revenue ($2013.496 million, as mentioned previously); the same is true of Tesla’s summed three-quarter 2014 gross profits ($616.974 million, loosely) and its total 2013 gross profit ($456.262 million). Regardless of what happens this Q4, then, Tesla’s annual revenue and gross profit has grown, indicating that the company is, at least for the moment, going up.

(click to enlarge)

Figure 3. Tesla’s annual income (in thousands), charted from 2010 through 2013. Note that 2013 saw an especially large year-over-year jump in gross profit; this is consistent with the behaviour of Tesla share prices in that year, as will be discussed soon.

Figure 4. Tesla’s quarterly revenues and gross profits have risen every quarter from Q4 2013 through Q3 2014.

Consumers’ increased demand for Tesla products (and, consequently, Tesla’s elevated production numbers) may also be attracting investors to the company, especially in the context of the immediate past: this Q3, despite a month of factory retooling earlier in July, the company reached its highest ever quarterly deliveries at 7,785 vehicles (with a significant year-over-year increase in demand, particularly in North America), and experienced a significant net increase in order numbers after slightly upgrading its Model S. As a result, Tesla has begun rescaling its production platform to increase Model S production speed, and forecasts a 50% increase in both net orders and deliveries for just that vehicle in 2015 (and “probably for years to follow”, according to CEO Elon Musk). Should this actually occur, Tesla’s top line – already growing steadily – could see even further success.

There is also the fact that Tesla is widely believed to have very little competition where luxury electric vehicles are concerned. As Stifel Nicolaus’ James Albertine sees it, by the time competitors even begin to develop a 250-mile-range vehicle (i.e., the kind of car that Tesla has already developed with the Roadster), Tesla may well have increased range; this claim coincides well, incidentally, with Elon Musk’s recent battery upgrade announcement, which suggests that Tesla is coming out with a 400-mile-range Roadster in the immediate future, and may well be dedicated to creating increasingly long-range battery packs for the Model S, X, and 3, which could lead to more and more practicality where EVs are concerned (and, consequently, more and more profit for Tesla).

In addition to the company’s core financial successes and its strong position in the electric vehicle industry, several recent business and product developments add momentum to the Tesla bullish case. Firstly, as was noted earlier, Elon Musk recently announced an upgrade to the Tesla Roadster that will allow the car – previously constrained to about a 250-mile range – to cover 400 miles on a single charge; this, in combination with Tesla’s global supercharger network plan and service centers, would electric vehicle (EV) driving less inconvenient, and thus more profitable for Tesla. Earlier this year, Tesla’s 2018 gigafactory plans – one of the “biggest projects it has ever pursued” – also generated investor interest and community support, creating jobs while fashioning a platform that will make Tesla production yet more sustainable. Finally, where large business developments are concerned, Tesla is interested in branching into emerging markets, the solar industry, and home automation; entering these new markets could, assuming the company somehow successfully lowers EV purchase and maintenance costs, contribute to company growth, as well.

Tesla’s organizational features – i.e., its operational methodology, professional relationships, leadership, and value-centric business philosophy – constitute another reason to side with the company. Firstly, Tesla’s sales schemes seem to be well-loved: some customers have called the Tesla purchasing experience “totally painless”, and the company presumably has 98% customer satisfaction (for perspective, note that Porsche comes in at a distant second at 70% customer satisfaction); this appears to be bred of the company’s innovative Another positive aspect of Tesla’s business model lies in its industrial diversity: while the company may, upon first glance, appear to focus solely on electric vehicle production, it also regularly engages in electric powertrain component deals with such large-scale automakers as Toyota and Daimler – a secondary focus which, given that it taps into another market without diverting Tesla’s central goal, seems sensible.

Tesla’s leadership, too, is widely cited in bullish analyses of the company. More specifically, CEO Elon Musk has been hailed as a genius where both entrepreneurship and engineering are concerned; Yahoo! Finance, for one, went so far as to suggest that Musk will be seen as a person who “really changed the world”, and will be historically significant. The whole of the company, in fact, could be seen similarly: with a focus on propagating sustainable energy, allowing technology patents to be essentially open-source, strategically creating jobs in needful areas, and optimizing customer satisfaction, Tesla appears to be in line with the kinds of progressive values that coincide with the mindsets of future generations; this is another reason that its long-term future appears sustainable.

And indeed, according to almost everyone commenting on Tesla, it is the company’s long-term stability that seems assured. Stifel Nicolaus’ James Albertine, for example, has stated that, even if Tesla does not enter China and does not reach the $400 per-share target he set for the company, it will still be a good investment in 2015 and beyond. Others second this sentiment, noting that Tesla dominance – even if it does not immediately occur – eventually will arise, and is worth waiting on.

Finally, one of Tesla’s largest strengths, perhaps, is that the company seeks to fix what isn’t working; this allows us to reconsider many of those claims made by advocates of a bearish Tesla. Some analysts were concerned earlier this month when it was announced that Tesla China’s new chief has resigned, citing two consecutive executive resignations – in combination with the Chinese government’s lack of incentive where electric vehicles are concerned – as evidence that Tesla China is not as stable as the company would like. As though in response, Tesla reported that it will help Chinese car owners trade in old vehicles if they buy the Model S, and that the value of their trade-ins could assist them in purchasing the Model S for a lower price. China by all means still represents a problem for Tesla – in fact, stock declined today by dint of the country’s imposing limits on EVs until 2020 – some problem-solving is better than none. On another occasion, critics pointed out that declining gas prices could influence EV sales, given that EVs would no longer necessarily be able to claim dramatically superior cost-efficiency. However, as many other analysts note, Tesla is not about cost-efficiency, dominantly: customers capable of and interested in purchasing a $100,000 car, firstly, may be less likely to be so concerned with a little excess cash going towards car maintenance and power (so, declining gas prices won’t seem enough of a “grab” for them to avoid a Tesla vehicle), and are, secondly, purchasing these cars for their customizability, low maintenance and operating service costs, updated technological capabilities, and futuristic appeal; as such, demand for Tesla is probably not going anywhere.

Analyst opinion appears to resonate with these positives: as has been noted, nearly all firms are at least slightly bullish on Tesla, even in the wake of the December drop. Stifel Nicolaus, as has previously been noted, upgraded its shares on December 26th; according to Bloomberg, of twenty-two analysts polled, thirteen advocate buying, and seven suggest holding. Dougherty and Company analyst Andrea James concurs, reiterating her outperform rating on Tesla, and citing Musk’s strategic work and Tesla’s innovative technology as the basis for Tesla’s strong sales in 2014. Tesla is so well-loved at the moment that some suggest it will be one of the most fast-forward moving stocks of 2015, starting the new year off strong, and surpassing the likes of Netflix, Google, and Apple as it seeks to reach its high target price. In some cases, the sentiment is near-extreme: CNBC, for example, has reported that some analysts believe Tesla will outperform every other stock in 2015.

Algorithmic Perspective

While algorithmic analysis is not to be considered conclusive, it is useful when combined with traditional techniques. Where such stocks as Tesla are concerned, algorithmic analysis – which relies upon historical trends and other information – can be especially useful in carefully piecing apart one’s investment decisions, which may otherwise be subjective to surrounding (in this case, overwhelmingly positive) bias.

I Know First is an investment firm that uses an advanced self-learning algorithm based on artificial intelligence, machine learning, and artificial neural networks to supplement its fundamental analyses. In doing so, it predicts the flow of money in almost 2,000 markets across a range of time frames (e.g., 3-days, 1-month, 1-year). It should be noted that the algorithm’s predictability (i.e., its accuracy) becomes stronger in 1-month, 3-month, and 1-year forecasts; as such, it can – when coupled with traditional analysis and careful reasoning – most effectively be used to analyze both short-term and long-term trends, but is not as convenient where intraday trading is concerned. The algorithm has seen a high degree of accuracy. As such, while it may seem tempting to disregard its predictions, cross-checking with its suggestions can be helpful in deciding where to place your money.

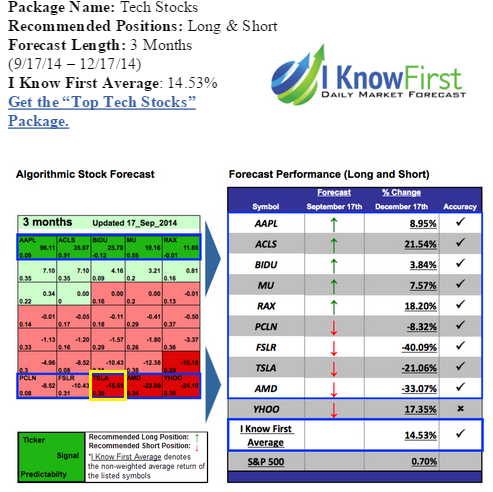

In particular, I Know First has previously helped investors decide how to engage with Tesla. Recently, in fact, the algorithm successfully predicted that Tesla would be bearish in the three-month time frame between September 17th, 2014 and December 17th, 2014: this forecast was accurate, as can be seen below, yielding returns of -21.06% (Figure 5).

Figure 5. Three-month forecast for Tesla, last updated September 17th, 2014; Tesla, boxed in yellow for emphasis, was deemed bearish (left), and this prediction coincided with its actual behaviour (right).

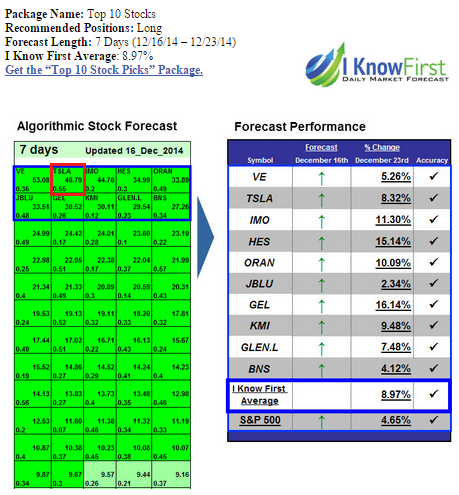

On a second occasion, the I Know First algorithm forecasted Tesla’s success in the seven-day time frame; albeit that the algorithm tends to get more accurate with month-plus long predictions, this forecast – running December 16th through December 23rd, 2014 – managed to understand the nuances of this year’s December drop: while many would have just termed Tesla bearish in the short term on December 16th, the algorithm was able to predict Tesla’s December 18th rise, for a return of 8.32% (Figure 6).

Figure 6. Seven-day forecast for Tesla, last updated December 16th, 2014; Tesla, boxed in red for emphasis, was deemed strongly (left), and this prediction – despite the fluctuating conditions of the stock in mid-December – coincided with its end behaviour (right).

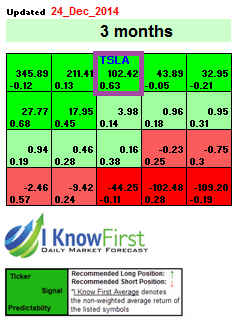

Given that the algorithm appears relatively accurate, then, its most recent Tesla-related forecast (Figure 7) – updated on December 24th, and spanning three months – is shown below. Bright green signifies a highly bullish signal; light green also indicates that the forecast is bullish, but not as strongly so. Bright red, in turn, signifies a bearish forecast; correspondingly, light red indicates a bearish forecast as well, but not as negative a forecast. Each compartment contains two numbers: the strength of the signal itself (represented by the number in the middle of each box, to the right), and itspredictability (found in the bottom left corner, this is the approximate level of confidence the algorithm has in the forecast).

Figure 7. Newly updated three-month forecast for Tesla, last predicted December 24th, 2014; Tesla, boxed in purple for emphasis, has been deemed strongly bullish in the months to come; this coincides with fundamentals.

Tesla’s position on the algorithmic chart, then, indicates a strongly bullish signal for the company in the three months to come; in the short term, of course, this signal may not be as accurate (right now, for example, on December 30th, Tesla is down), but this appears to coincide well with longer-term (i.e., three month) business developments discussed earlier.

Conclusion

While Tesla Motors, Inc. may have experienced a minor drop in share price in recent months, it is still very much a force to be reckoned with. Bringing to the table a combination of consistent revenue and profit growth, elevated production goals, lack of competition, recent business developments, unique organizational structure and leadership, and ability to problem-solve, the company is also focused on customer satisfaction and environmental sustainability: two values that are integral to attracting precisely the kind of strong following that Tesla – despite its lack of advertising, mind – already possesses. While Tesla stock may well fluctuate over the course of a few days, then, Tesla’s all about electricity, so its success should, like electricity, come in waves. Ride that turbulent breaker right through, and you’ll find yourself swimming in opportunity.

Business relationship disclosure: I Know First Research is the analytic branch of I Know First, a financial start-up company that specializes in quantitatively predicting the stock market. This article was written by Sophia Glisch, an I Know First intern, and edited by Daniel Barankin, our International Business Development Project Manager. We did not receive compensation for this article (other than from Seeking Alpha), and we have no business relationship with any company whose stock is mentioned in this article.